By Cris Alarcon, InEDC Writer. April 4, 2026)

EL DORADO COUNTY, Calif. —

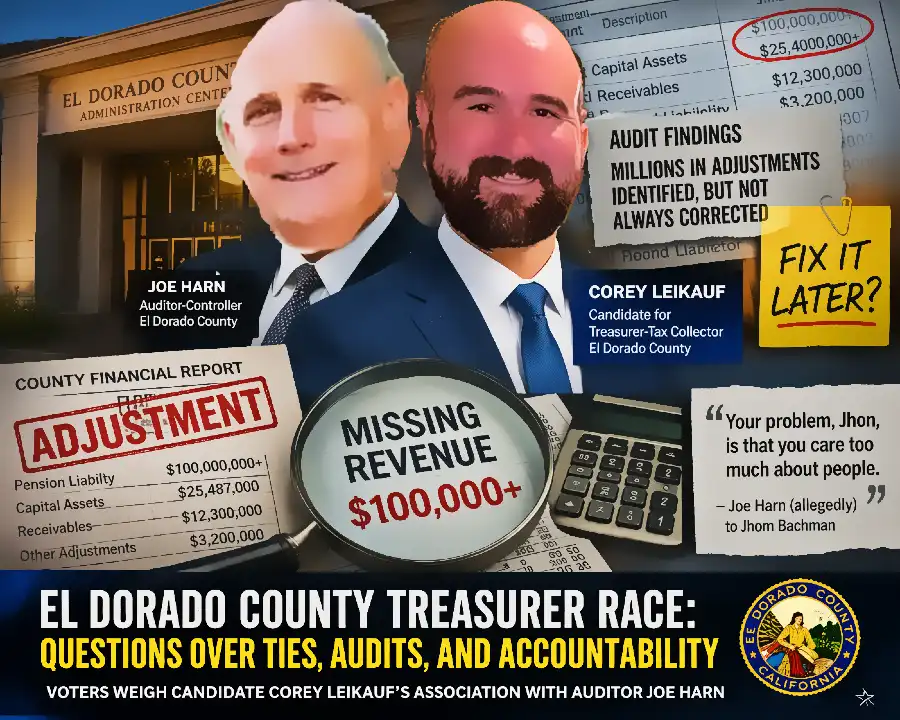

A developing political question in El Dorado County’s Treasurer-Tax Collector race is whether candidate Corey Leikauf could face electoral headwinds due to his professional association with longtime Auditor-Controller Joe Harn, as critics point to a history of accounting concerns raised in past audits and internal reports.

The issue has gained traction following commentary from local watchdog group El Dorado County Government Watch, which alleges a pattern of delayed or incomplete financial corrections within county government over multiple years. The group cites prior audit findings indicating that certain accounting discrepancies — including capital asset valuations and receivables — were identified but not always promptly recorded.

Publicly available financial audits of El Dorado County have, at times, documented material adjustments made during external review processes. In one instance referenced by critics, auditors identified a significant liability adjustment related to retiree benefits exceeding $100 million. While such adjustments are not uncommon in government accounting, they have been used by detractors to argue that internal controls may have relied heavily on post-audit corrections rather than proactive reconciliation.

“These issues reflect a pattern where errors are often discovered during audits rather than through internal controls,”

the watchdog group wrote in a recent statement, adding that some discrepancies were

“corrected while others were deferred.”

The scrutiny extends beyond formal audits. Local accounts describe operational challenges within county departments, including a reported breakdown in coordination between service tracking and billing systems within Health and Human Services roughly a decade ago. According to individuals familiar with the matter, the disconnect may have contributed to missed reimbursements exceeding $100,000 in federal funds.

Former department leadership, including John Bachman, was reportedly unable to reconcile completed services with billing data due to separate systems that did not interface. An outside accounting review allegedly identified delays that rendered certain claims ineligible for reimbursement under federal timelines.

No independent audit report reviewed by this publication directly attributes that specific loss to misconduct; however, the anecdote has resurfaced in recent weeks as part of broader criticism of the county’s historical accounting practices.

More recently, community member Kimberly Hopkins Preston publicly questioned Leikauf’s qualifications and proximity to Harn’s office.

“Red flags go up when someone who works in his department, who lacks the experience and credentials needed to serve our county, is running for an elected department head position,”

Preston wrote.

“Be diligent in your research for the upcoming local election.”

Leikauf has not publicly responded in detail to these specific criticisms as of this writing. It also remains unclear whether his campaign will directly address concerns tied to Harn’s tenure or instead emphasize his own qualifications and policy priorities.

Harn, who has served as Auditor-Controller for decades, has not issued a recent public statement regarding the allegations circulating in connection with the Treasurer-Tax Collector race.

Context and Stakes

The Treasurer-Tax Collector plays a critical role in managing public funds, investments, and tax collection processes for El Dorado County. Voter confidence in financial oversight is often a decisive factor in such races, particularly in jurisdictions where prior audits have highlighted internal control challenges.

Political analysts note that association alone does not determine electoral outcomes. However, in local races — where professional networks are often closely scrutinized — perceived continuity with past administrative practices can become a central campaign issue.

Whether the concerns raised will materially impact Leikauf’s candidacy remains to be seen. Much may depend on voter awareness, campaign messaging, and whether additional documentation or official responses emerge in the weeks ahead.

Personal Disclosure — I have personal involvment in one fiasco. Almost a decade ago Our former head of Health and Human services John Bachman was at a loss of county revenues. One government funded program that was reimbursable was not reimbursed. It was because the billing was late in processing.

I became aware of this and got in touch with a friend Raphael Metzgar that was an accounting expert in Federal Accounting. He discovered that because of the was our county accounting was processed there was no way for Bachman to know what had been fulfilled and was due to be billed. This was because the two parts, what was done and what was billed were not connected. There was no way for the Department Head to access both systems. Raphael went into county records and found this system failure and explained it to Joe Harn. Joe’s response was “How do you know this? Rafael explained that he had downloaded both records onto a Excel and then Merged them to see there was delayed information about when service was rendered for so long that the billing was stale dated making the reimbursement void. This cost the county taxpayers over $100,000. When Health Department Head John Bachman confronted Auditor Joe Harn with this loss due to this county accounting deficiency, Harn repied, “Your problem John is that you care to much about people!” John Bachman is still a county employ and can confirm these facts. Raphael Metgar in currently in the hot zone in the Middle East doing Auditing work for the State Department execution of Trump’s efforts there.

{kind=link}