By Cris Alarcon, InEDC Writer. May 11, 2026

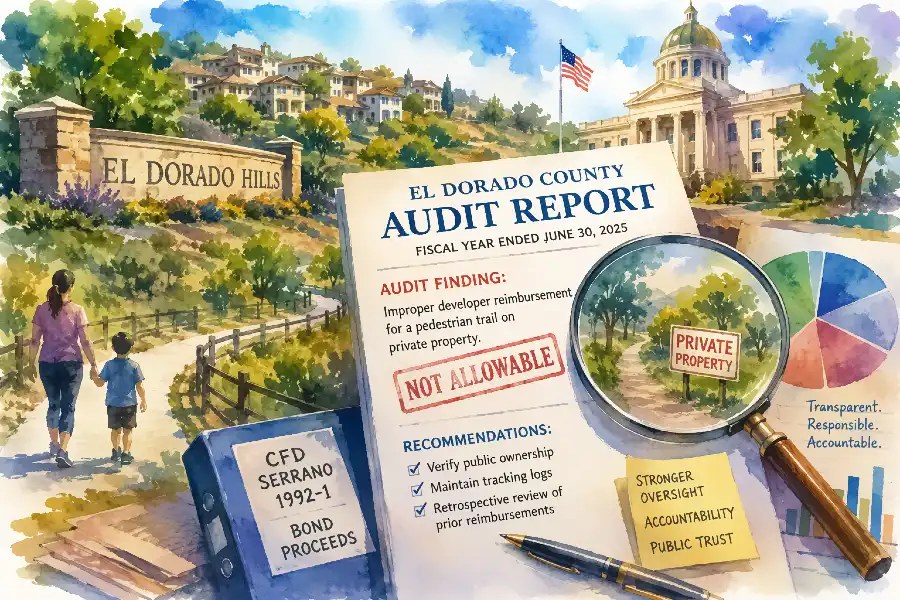

EL DORADO COUNTY, CALIFORNIA. An independent audit presented to the El Dorado County Board of Supervisors this week identified a significant internal control concern involving developer reimbursements paid through Community Facilities District bond proceeds in El Dorado Hills.

The finding appears within management reports prepared by Lance, Soll & Lunghard, LLP as part of the county’s fiscal year 2024-25 financial audit process. According to the auditors, the county’s Auditor-Controller approved reimbursement payments to a developer for construction of a pedestrian trail later determined to be located on private property and therefore not eligible under county reimbursement guidelines.

Auditors wrote that the reimbursement process for CFD expenditures originates within the county’s Department of Transportation before moving through multiple layers of review, including the County Engineer, the Chief Administrative Office Fiscal Unit, the DOT director and County Counsel before final approval by the Auditor-Controller.

“Recently, however, based on inaccurate written representations submitted by DOT, the Auditor-Controller reimbursed a developer for a pedestrian trail on private property, which was not allowable under the County’s reimbursement guidelines,”

the auditors stated in the report.

The issue involved CFD Serrano 1992-1 activity, a long-running financing district associated with infrastructure development in El Dorado Hills. Community Facilities Districts, commonly known as Mello-Roos districts, are financing mechanisms used to fund public infrastructure tied to new development.

Although auditors stopped short of issuing a formal reportable finding, they recommended significant changes to the county’s oversight structure. Those recommendations include independently verifying public ownership before releasing CFD funds, maintaining detailed reimbursement tracking logs and conducting a retrospective review of previous developer reimbursements to determine whether other payments complied with county policy.

The auditors also recommended that the county

“implement a comprehensive tracking log for all reimbursements and capital asset purchases made with bond proceeds to facilitate ongoing monitoring and accountability.”

The broader audit otherwise delivered a largely clean review of county financial statements for the fiscal year ending June 30, 2025. Auditors reported no identified misstatements, no disagreements with management and no significant difficulties encountered during the audit process.

The report also noted the county implemented Governmental Accounting Standards Board Statement No. 101 involving compensated absences during fiscal year 2025.

The audit documents were placed on the May 12 Board of Supervisors consent calendar under File No. 26-0775 through the county’s online legislative portal.

Public records for the agenda item are available through:

El Dorado County Legistar File 26-0775

{kind=link}